Veterans transitioning to federal civilian employment have a financial decision that should rank in the top three of their first year: whether to buy back military service for FERS pension credit. The math is almost always positive ROI by 10x-40x, and the window for paying the deposit at the lowest cost expires two years after federal hire.

Despite this, a substantial portion of veteran federal employees never complete the buyback. Some are unaware of the option. Some defer the deposit because the upfront cost feels significant. Some get bad advice from financial advisors who don’t understand federal retirement.

For veteran federal employees making this decision, here’s the math with realistic numbers.

How the Buyback Works

The mechanics:

- You served on active duty for some period (or earned creditable military service through Reserve activations)

- That military service didn’t result in a 20-year retirement (you weren’t already drawing military retired pay)

- You enter federal civilian employment under FERS

- You request a deposit calculation from your federal HR or directly through OPM

- You pay the deposit (roughly 3% of your basic military pay during those years)

- Your military years count toward FERS pension calculation and eligibility

The deposit cost is calculated based on:

- Years of active military service

- Basic pay rate during each year

- 3% rate (3.0% for service before 1999, varies for post-1999 service)

- Plus interest if more than 2 years past your federal entry-on-duty date

The Two-Year Window

The most expensive mistake veterans make: deferring the deposit calculation past the 2-year window.

For deposits paid within 2 years of federal start date: no interest accrues. Your cost is the simple percentage of military base pay.

For deposits paid after 2 years: interest accrues on the unpaid balance, compounding annually. The interest rate is set by OPM and has historically run 4-6%.

Concrete example: an Army E-5 with 8 years of service. The base 3% deposit might be roughly $9,500. Paid within 2 years: $9,500. Paid 10 years after federal start: $9,500 plus 8 years of compound interest = roughly $14,500-$16,000.

The math is still positive ROI even with the interest penalty, but the early-payment window saves real money. Plan the deposit in the first year of federal employment.

The Lifetime ROI Calculation

Walking through specific examples for typical veteran federal employees:

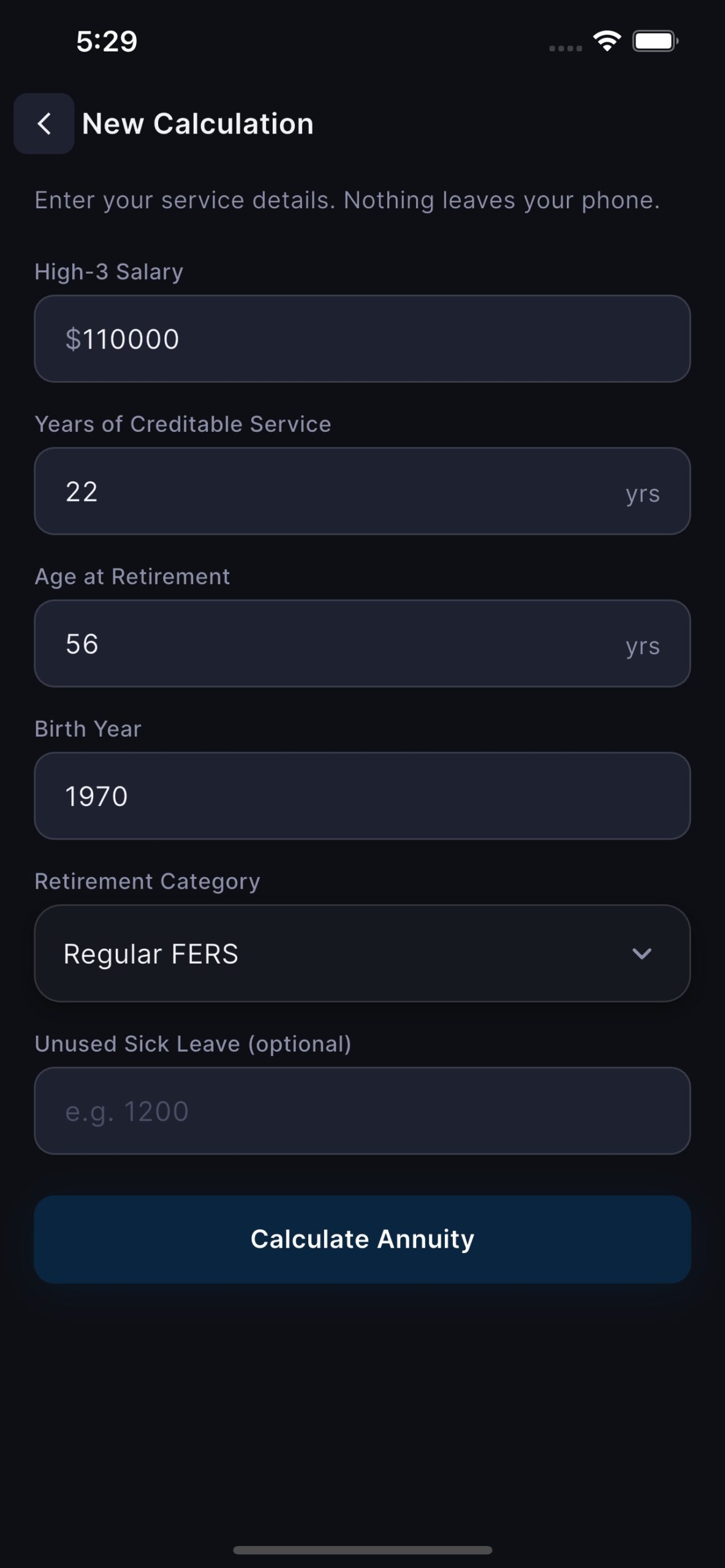

Example 1: E-5 veteran, 6 years military, GS-11 federal employee, retires at 30 years federal service (so 36 years total).

- Without buyback: 30 years × 1.0% × high-3 ($110,000) = $33,000/year

- With buyback: 36 years × 1.1% (62+ age multiplier) × $110,000 = $43,560/year

- Annual difference: $10,560

- Over 25-year retirement at 3% COLA: roughly $310,000 additional lifetime pension

- Buyback cost (within 2 years): roughly $5,500

- ROI ratio: ~56x

Example 2: O-3 veteran, 10 years military (no military retirement — left at 10 years), GS-13 federal employee, retires at 28 years federal service (so 38 years total).

- Without buyback: 28 years × 1.0% × $135,000 = $37,800/year

- With buyback: 38 years × 1.1% × $135,000 = $56,430/year

- Annual difference: $18,630

- Over 25-year retirement at 3% COLA: roughly $550,000 additional lifetime pension

- Buyback cost (within 2 years): roughly $18,000-$22,000

- ROI ratio: ~25-30x

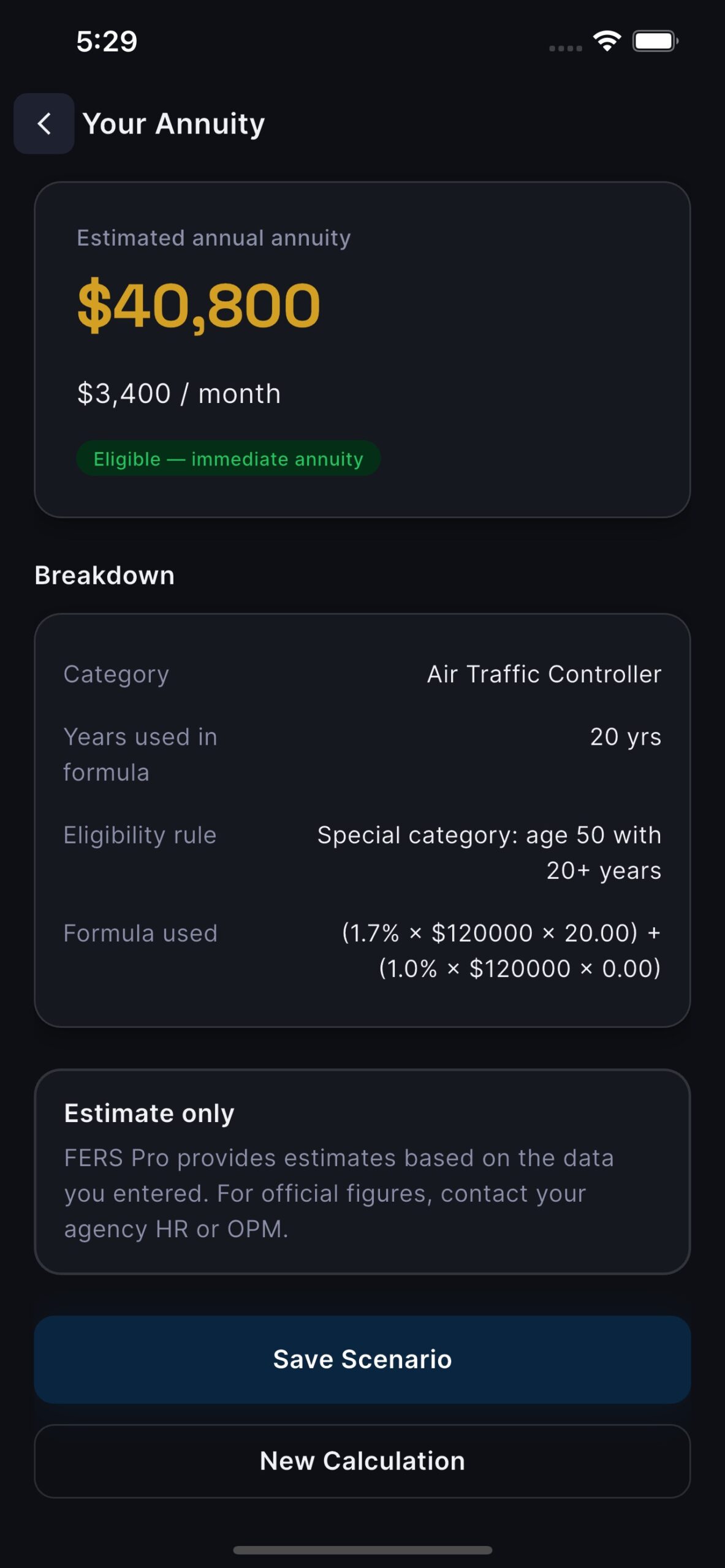

Example 3: E-7 veteran, 14 years military (no retirement — separated at 14), GS-12 federal employee, retires at 18 years federal service (so 32 years total).

- Without buyback: 18 years × 1.0% × $120,000 = $21,600/year

- With buyback: 32 years × 1.1% × $120,000 = $42,240/year

- Annual difference: $20,640

- Over 25-year retirement at 3% COLA: roughly $610,000 additional lifetime pension

- Buyback cost (within 2 years): roughly $14,000-$18,000

- ROI ratio: ~35-40x

The pattern: across realistic scenarios, the buyback ROI is consistently 20-50x. There are very few financial decisions with this magnitude of upside relative to upfront cost.

The Exceptions Where Buyback Doesn’t Apply

A few specific situations where the buyback isn’t available or doesn’t make sense:

1. You’re drawing military retirement. If you completed 20+ years and are receiving military retired pay, your military years can’t be bought back for FERS — that would be double-counting. The exception: you can waive military retirement to buy back, but this is almost never a good trade.

2. You served only Reserve/Guard time without activations. Inactive Reserve time doesn’t count for the buyback. Only active duty service (including activated Reserve/Guard time) qualifies.

3. You were separated under conditions other than honorable. Various-discharge categories may not qualify. The eligibility is the same as for other VA benefit eligibility.

4. You’re already past the federal retirement decision point. If you’re 65+ and 30+ years federal service, the math may be less favorable due to limited remaining retirement period. Still usually positive but smaller margin.

The Payment Mechanics

The deposit can be paid in three ways:

1. Lump sum. Pay the full deposit at once. Simplest mechanically.

2. Installments via payroll deduction. Most federal HR offices can set up payroll deductions for the deposit. Spread over months or years until paid.

3. Combination. Partial lump sum plus payroll deductions for the remainder.

For deposits under $5,000, lump sum is usually feasible. For larger deposits, payroll installments are more manageable. The total cost is the same either way as long as you complete payment within the 2-year window.

Common Reasons Veterans Skip the Buyback

Patterns from talking with veteran federal employees who didn’t complete the buyback:

1. “I didn’t know about it.” The most common reason. Federal HR generally informs new hires of the buyback option but the explanation often happens during the firehose of onboarding and gets lost.

2. “It seemed expensive.” Looking at a $10,000-$20,000 deposit feels significant in the first year of federal employment. The ROI calculation isn’t usually done.

3. “I’ll do it later.” Deferred past the 2-year window. Now subject to compound interest.

4. “A financial advisor told me not to.” Financial advisors who don’t understand federal retirement sometimes treat the deposit as a cash outflow without understanding the lifetime pension impact. Get federal-retirement-specific advice before deciding.

5. “I’m planning to leave federal employment.” Even if you leave federal employment, the deposit you made counts toward any future FERS-eligible federal service if you return. Worst case, you can request a refund of the deposit (without the pension credit).

What to Do This Year if You’re a Veteran Federal Employee

Three actions if you’ve never run the buyback math:

1. Request the deposit calculation. Submit Form RI 90-1 (Application to Make Deposit) through your federal HR or directly to OPM. Free, gives you the exact cost.

2. Run the lifetime pension comparison. Use the FERS calculator with and without the buyback years. The ROI ratio is usually obvious once you see the numbers.

3. Pay the deposit within the 2-year window if positive ROI. Lump sum if you have cash; payroll installments if not. Either way, complete the payment before the interest-free window closes.

For the broader FERS retirement calculation including MRA decisions and FERS supplement timing, see the FERS Pro federal retirement guide.

Leave a Reply